.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

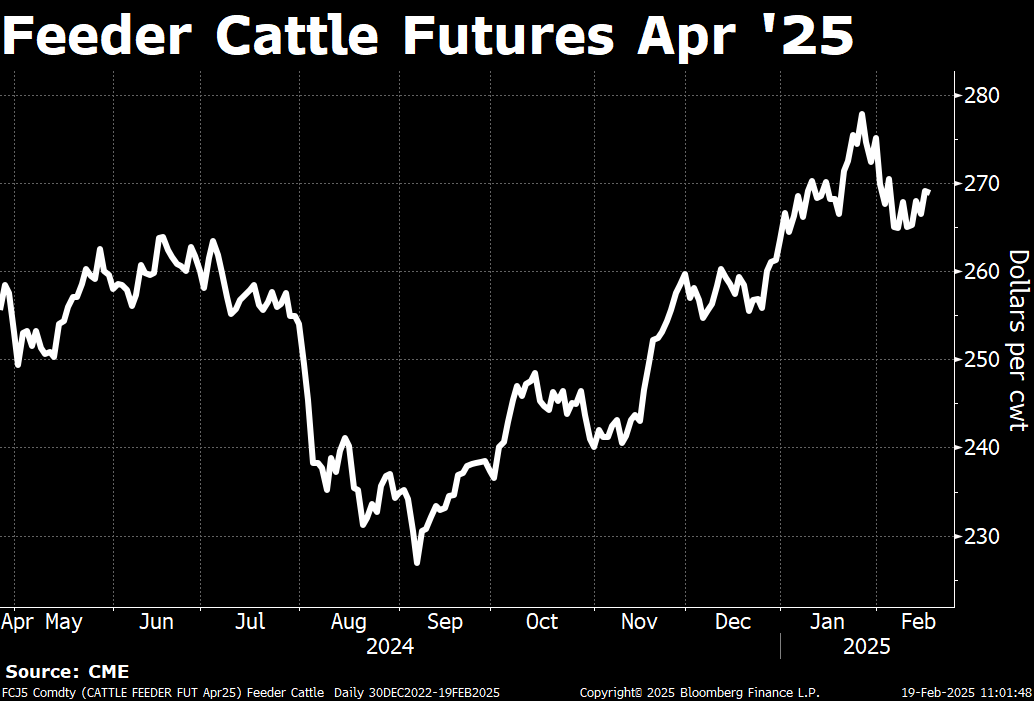

The cattle markets have exhibited many mixed tones this week. One day, feeders are surging and live cattle are lower. The next day, it’s the opposite.

Typically, when there is a divergence in price action between the two, the market hints at the next direction it plans to go.

Over the past week, feeder cattle have held up better than live cattle after finding support early last week. If the saying, “feeders are the leaders,” provides any insight, we could assume the market is set for more sideways trade, as Chad Toyne suggested in his most recent broadcast.

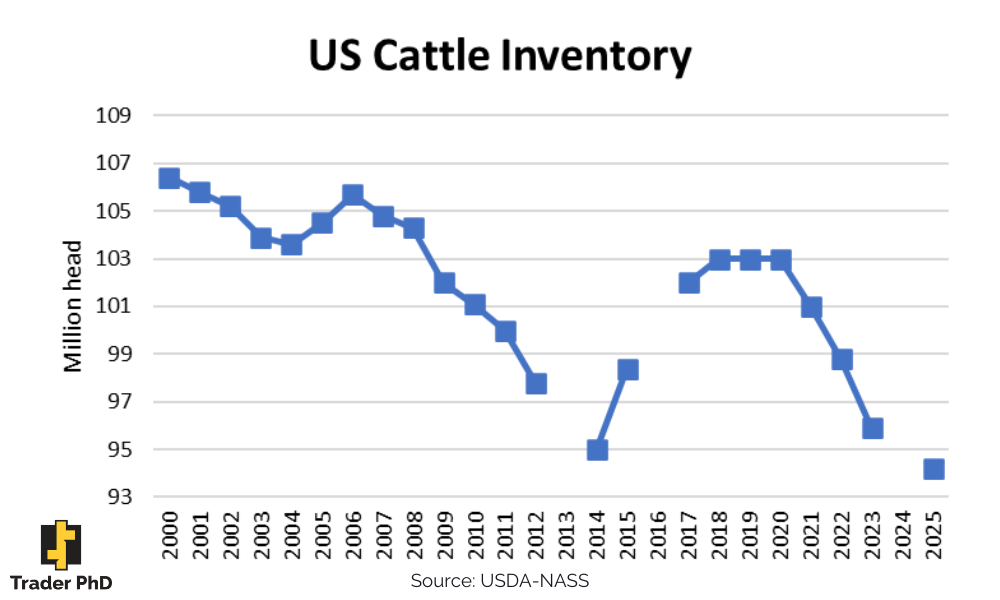

Most of last week’s selloff in the live cattle market was driven by long liquidation as speculators cashed in profits following record-high prices. The move correlated with the USDA’s annual cattle inventory report, which confirmed tighter U.S. supplies and little excitement for herd expansion.

Fundamentally, nothing has changed in the current U.S. supply besides the USDA reopening the border to cattle imports from Mexico. The restart process is expected to be slow due to additional steps for importers bringing cattle north of the border.

The focus is turning back toward the monthly data, where the USDA’s February Cattle on Feed report will give us the most recent data on feedlot trends.

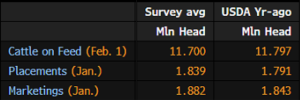

Ahead of the report, a Bloomberg survey of analyst estimates predicts the Feb. 1 feedlot inventory to total 11.7 million head, down nearly one percent from last year.

Source: Bloomberg

Placements are expected to have increased by 2.7 percent from last year to 1.839 million head. The resumption of feeder cattle imports from Mexico could help placements recover after falling to the lowest December print since 2015.

Fed cattle marketings for January are expected to total 1.882 million head, up 2.1 percent from a year ago. If realized, that would be the strongest January print since 2019.

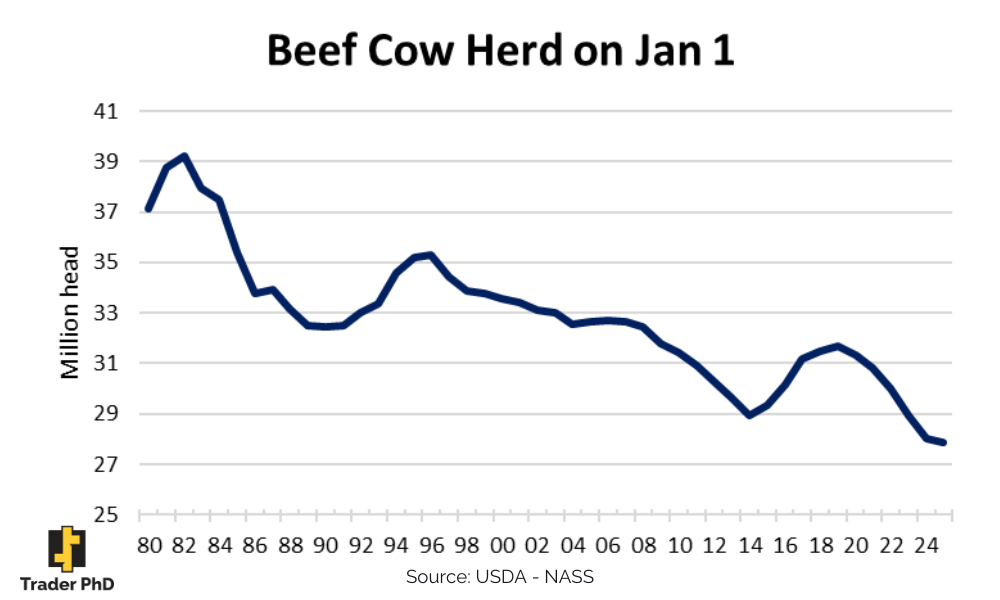

Monthly data shows a steady feedlot cattle supply compared to a year ago. However, feeder cattle supplies are lower, and there are fewer cows and heifers to rebuild supplies.

It’s hard to say the bull market is over considerably the historically tight supplies. That doesn’t mean we won’t see any corrections - it happened multiple times before the end of last year.

Let’s not forget about the consumer's resilience with elevated retail beef, either.

Want to receive more commodity-related information? Sign up for a free trial to stay up-to-date on the latest market trends.