.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

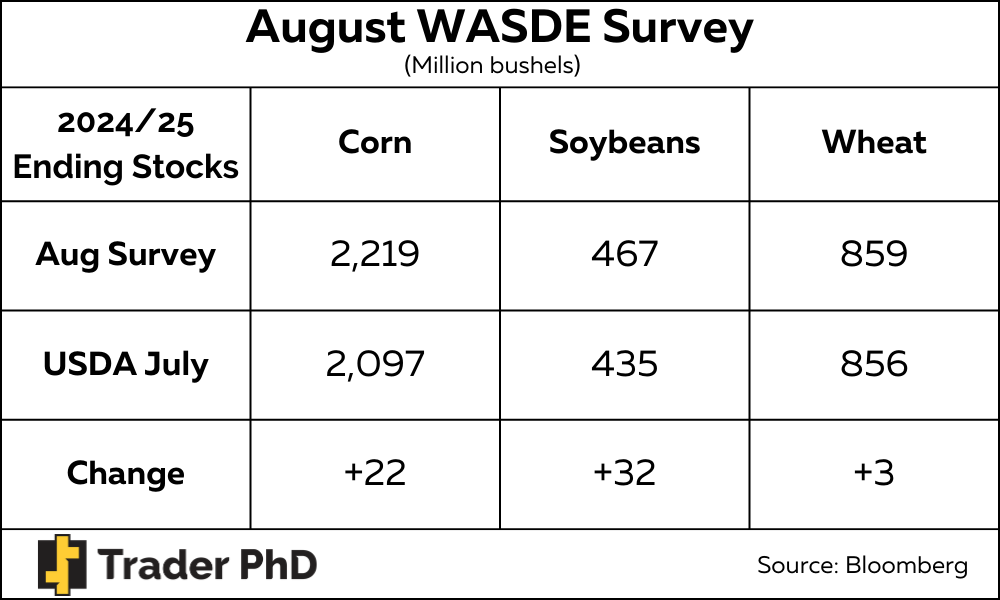

The USDA will release its final WASDE report during the 2023/24 marketing year on Monday and will provide an updated 2024/25 balance sheet for corn, soybeans, and wheat.

Traders are not expecting a significant change for corn and wheat ending stocks compared to the July report. However, the new crop soybean carryout continues to get larger and closer to levels last seen in 2019/20.

CORN

A monthly Bloomberg survey predicts that the 2024/25 corn carryout will be raised by 22 million bushels from July to 2.219 billion. An increase in the USDA’s forecast would likely come from an increase in production due to higher yields.

Whether the USDA will adjust its planted or harvested acres based on prevent plant has yet to be realized. The Farm Service Agency will release its Acreage Certification Update report on Monday, will should be about 80 percent complete, and any clear signs of variance from the June Acreage report could warrant an adjustment in Monday’s WASDE.

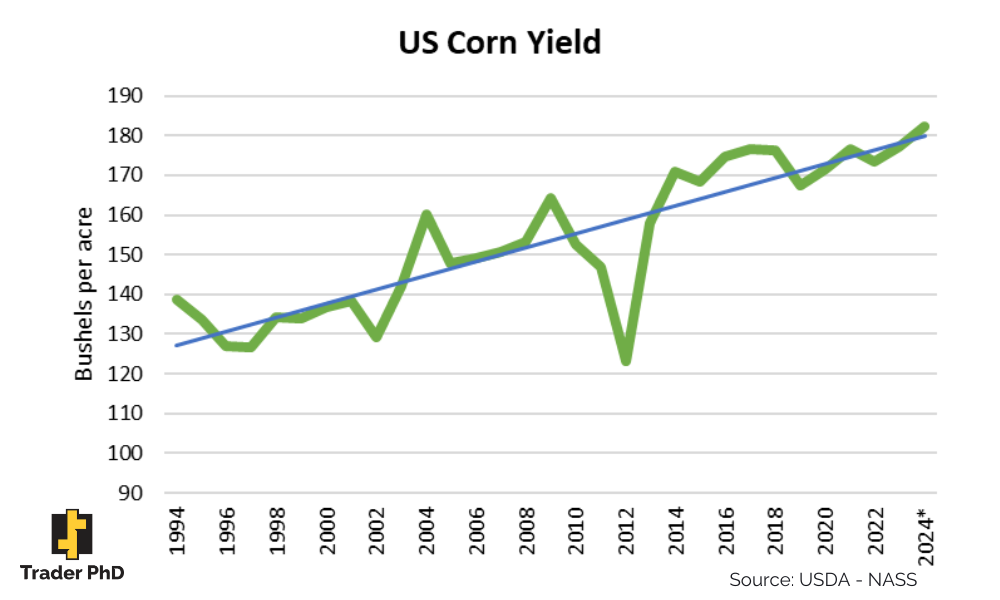

Otherwise, corn yield is expected to come up to 182.2 bushels an acre, compared to 181 in July. The market is seemingly pricing in an above-trendline yield as fields in the Eastern Corn Belt are expected to offset production issues in other areas. Total output is expected to be 15.12 billion bushels, up 23.7 million and just behind last year’s record of 15.3 billion.

SOYBEANS

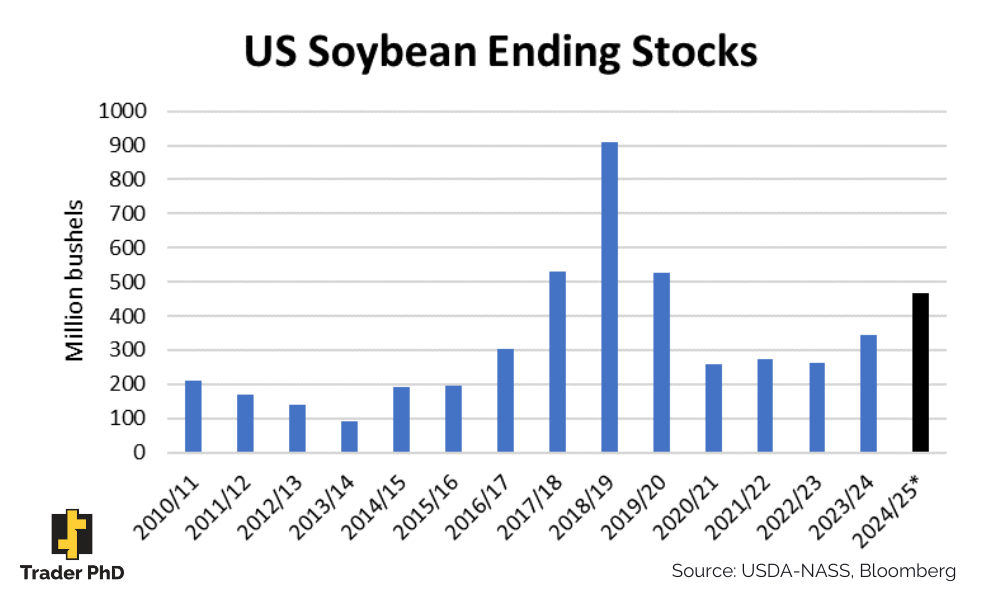

Traders expect soybean ending stocks to come in on the bearish side this month and are expected to rise 32 million bushels from July to 467 million. The 2024/25 carryout could get a boost from higher production estimates yield could come up from the previous month.

Soybean production is expected to be 4.48 billion bushels, up 36.5 million from last month. Yields are expected to be up 0.5 percent at 52.5 bushels an acre. But, with rising production and falling demand, soybean supplies continue to become more burdensome, with stocks projected at a five-year high. Soybean stocks-to-use are projected to be around 10 percent, a far cry from six percent coming out of the pandemic.

The USDA’s latest export sales data showed a large bump in new crop soybean sales compared to previous weeks. However, outstanding sales for 2024/25 are down 50 percent compared to the previous year during the same period.

Even as China shows better demand for U.S. soybeans, total bookings account for less than five percent of last year’s pace as of Aug. 2. And I wouldn’t bet on an increase in U.S. soybean demand unless it comes from domestic crush.

WHEAT

World wheat prices received a boost in May after adverse weather in the Black Sea and pre-harvest expectations in the U.S. led to strong short covering in the wheat complex. However, that bullish sentiment dissipated throughout July, leading to new contract lows. Fortunately, Monday’s WASDE might not offer much extra bearish sentiment, with the 2024/25 carryout expected to be raised slightly to 859 million bushels.

However, the monthly Crop Production report, also set for release on Monday, could come with a bump in the wheat production forecast, according to a Bloomberg survey. The average analyst guess predicts all wheat production up 9.1 million bushels from July to 2.017 billion. The increase would be driven by a bump in winter wheat output.

Noncommercial traders currently hold a large net short position heading into the report as corn and soybean futures trade at or around recent lows. December corn futures have been reluctant to trade much below $4 a bushel, but downward momentum continues to keep the pressure on prices. It’s no exaggeration that the mood for corn and soybean prices is bearish as the end of the marketing year nears.

Want to receive more commodity-related information? Sign up for a free trial to stay up-to-date on the latest market trends.