.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

The U.S. hog market has had its ups and downs over the past few years following the post-pandemic bull market. That has led to wide profit swings, though farrow-to-finish operations have favored better than feeder-to-finish. Hog prices have recovered over the past year, though production expenditures have limited returns.

Struggling Margins

According to Iowa State University, producers in Iowa have sustained positive margins since April after live hog prices began to increase in March. Economists calculated that the typical farrow-to-finish operation averaged a profit of $7.76 per hog in September. That was the lowest return since producers became profitable again this year. Still, that was a far cry from when losses reached a record in 2023 for data from 2002 after hog prices fell significantly from their multi-year highs.

Feeder-to-finish margins faced more pressure, with returns closing out last month at a loss of $0.10 per head. That was the third consecutive month of negative returns, but still not as bad as earlier last year. Pork packer margins have seen their fair share of volatility. Returns have been positive for most of the past year, aside from a dip into negative territory in July. Estimated margins from HedgersEdge are floating around $30 per head. An adequate supply of market-ready hogs in the U.S. will likely support packer returns.

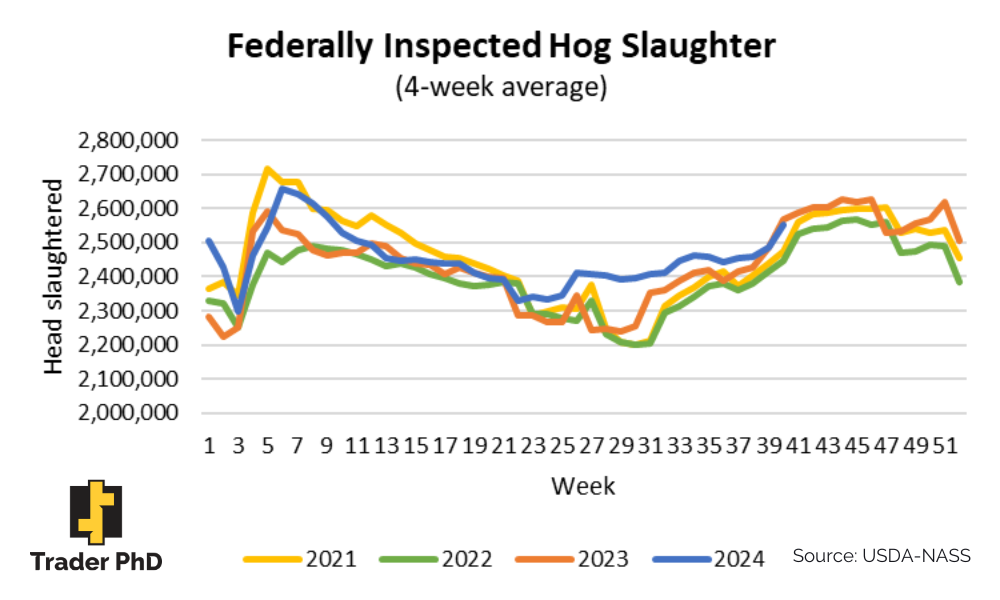

Strong Hog Slaughter

Slaughter rates have run at full speed for most of the year to take advantage of adequate supplies. Meatpackers have been working to keep up with domestic and international demand. Federally inspected hog slaughter for the first 40 weeks through September totaled about 98.2 million head, up 1.5% year-over-year. Pork production rose 1.7% to 20.95 billion pounds as higher hog weights added to increased supplies. Declining feed prices will likely keep weights elevated.

U.S. sow slaughter was down about 1% for the first nine months of the year, according to weekly USDA data. Monthly numbers showed that slaughter for the first half of the year was at the highest pace since 2020 when producers were liquidating herds amid the Covid-19 pandemic. However, volumes have since declined and are reverting back to more normal levels.

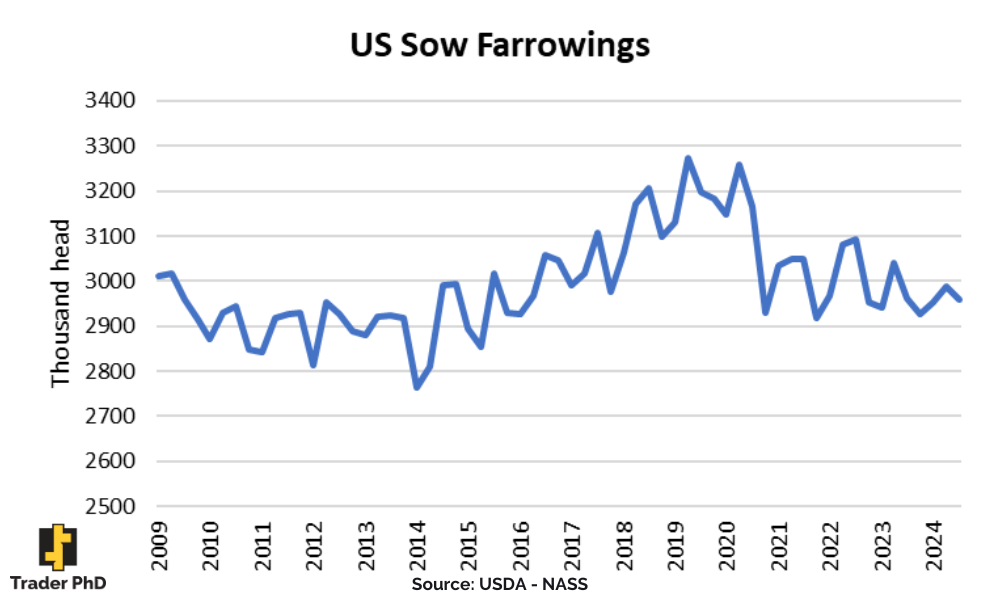

The pandemic significantly reduced sow farrowing, and strong sow slaughter over the past two years has prevented farrowings from recovering, as the USDA’s Quarterly Hogs and Pigs report indicates. Increased pigs per litter have helped offset lower farrowings, which has kept plenty of pigs in the pipeline.

Report data has suggested that higher pig crop numbers have continued as producers culled the least productive sows and brought in more productive gilts, increasing overall herd productivity. The September report showed a 0.8% decline in the pig crop, the first year-over-year decline in three quarters. If the number of pigs per litter peaked, a continuation of herd liquidation could mean fewer pigs in the pipeline down the road.

Demand

Pork has benefited from favorable domestic and international demand this year as beef prices remain high and, poultry is elevated due to the effects of Highly Pathogenic Avian Influenza. Per capita consumption is expected to reach 50.9 pounds, an improvement from 2023.

Exports have been the brightest spot for the industry. Last year, pork and pork product exports totaled 2.91 million metric tons, reaching a record value of $8.17 billion. Much of that momentum continued this year, with shipments through August up 4.4% year-over-year.

Mexico has been the primary driver of exports, with year-to-date shipments up 8% from a year ago. However, increased demand in other markets, such as Asia and Oceania, has helped drive larger exports.

Conclusion

The USDA forecasts pork production to reach a record 28 billion pounds in 2024. Strong international and domestic demand has helped prevent pork inventories from reaching a supply glut. While producers have seen better hog prices this year, high production costs have limited profits. Feed costs have had less pressure on operations after falling to pre-pandemic levels this summer and offering some buying opportunities. The USDA forecasts hog prices to soften in the first half of 2025 due to strong expected competition with beef and poultry.

Here’s a note from an article we put out last October. “The pork industry is resilient, and the market often finds a way to balance itself. The 2023 season came off two years of high prices that led to strong returns. As producers face challenges now, that gives way to better times ahead.”

We began to see the re-balancing occur this year. Livestock production is a margin game, and as we reflect on the industry during National Pork Month, the hard work producers put in to protect their livelihood is hard to match.

Want to receive more commodity-related information? Sign up for a free trial to stay up-to-date on the latest market trends.