.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

Fertilizer prices have been trending higher across multiple categories despite U.S. demand tapering off into a seasonal lull.

On average, wholesale fertilizer prices are up nearly 25 percent since the start of the year, according to the Green Markets North American fertilizer price index.

What’s driving higher prices?

Prices have been sticky for producers despite declining crop prices. Recent tensions in the Middle East have garnered significant attention this year. Israel and Iran’s missile strikes at one another and, eventually, the U.S. bombing Iranian nuclear sites sent wholesale urea prices surging this spring.

The announcement of a ceasefire between Israel and Iran helped prices cool, but they are now $75 higher than they were a month ago.

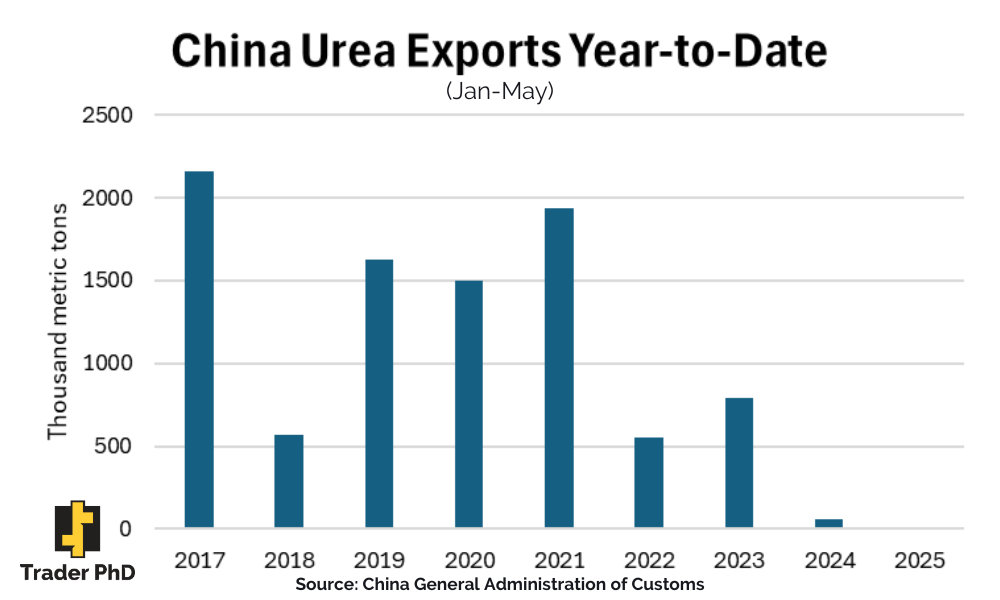

What has received less attention is China’s absence in the global marketplace. China has placed major restrictions on fertilizer exports to ensure adequate supplies to increase domestic crop production. In 2021, China exported about 5.3 million metric tons of urea, according to Chinese customs data. In 2024, they only exported about 250,000 metric tons, with no shipments reported for 2025.

High tariffs on phosphate imports from Morocco have limited supplies. In 2021, Morocco accounted for 38 percent of U.S. phosphate imports. Since 2022, shipments from the country have averaged about three percent of total imports.

U.S. corn acreage is estimated to be about a record this season, with farmers having planted about 95.3 million acres, according to the USDA. Additionally, increasing corn acres in Brazil have been another driver of demand in the Americas over the past decade.

Fertilizer trade impacts

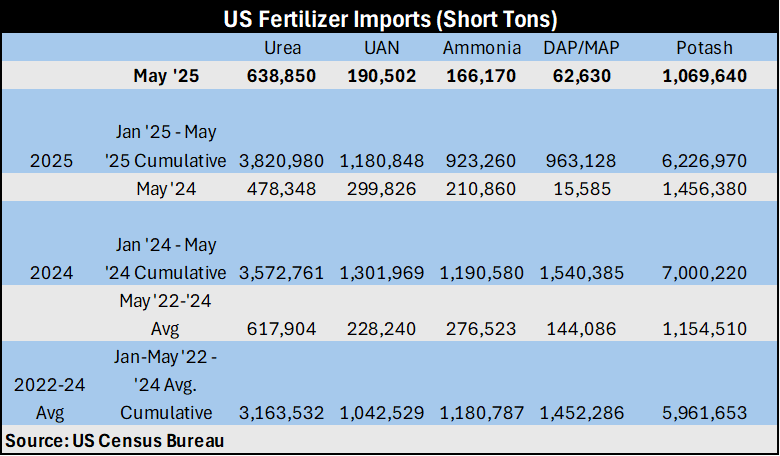

Fewer supplies leaving China have left many countries in a pinch, including the U.S. Below are tables highlighting monthly fertilizer import data from the U.S. Census Bureau.

Notably, nitrogen and phosphorus imports have been declining over the past few years, with the exception of urea. UAN imports for the first five months of 2025 totaled 1.18 million tons, down nine percent year-over-year. Year-to-date phosphate imports are 37 percent lower than last year at 963,000 tons and were the lowest through May since 2015.

Saudi Arabia has accounted for 37 percent of total U.S. phosphorus imports over the past year and has been the top supplier for the U.S. Canada has been the top origin of nitrogen and potassium imports.

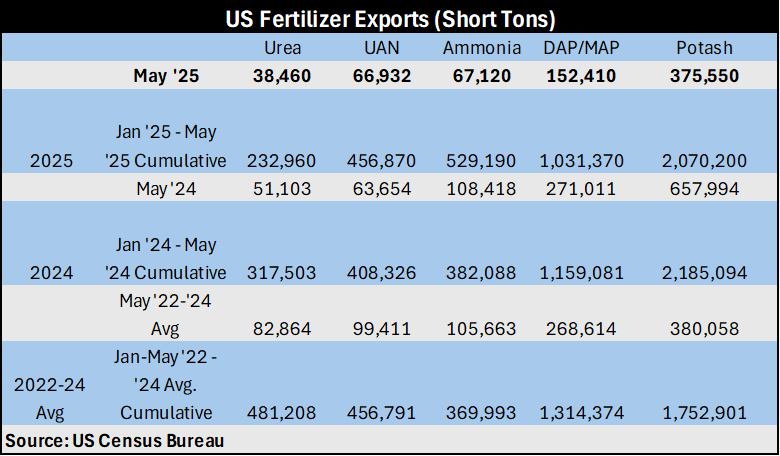

Phosphate exports have been declining due to falling inventories. Year-to-date exports are 11 percent lower than last year and 22 percent below the three-year average for the same period.

Affordability pressures grow

Affordability has worsened as fertilizer prices climb while crop prices fall.

- DAP is among the least affordable, with wholesale prices reaching their highest level since September 2022.

- Urea has become more competitive compared to UAN, prompting a shift in application strategies.

- Potash remains the most affordable, thanks to somewhat stable trade with Canada.

Tariff uncertainty could continue to support fertilizer prices, as well as restricted global export flows. Remaining in close contact with fertilizer suppliers will be key to taking advantage of pricing opportunities if they arise.

Want to receive more commodity-related information? Sign up for a free trial to stay up-to-date on the latest market trends.

--

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. FUTURES TRADING INVOLVES SUBSTANTIAL RISK AND IS NOT SUITABLE FOR ALL INVESTORS.