.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

Corn futures have been in the doldrums lately, but falling prices are not being met with lower demand.

In a previous special report, we identified that Grain stocks are becoming more burdensome. Naturally, prices have been declining due to fundamentals of rising supplies.

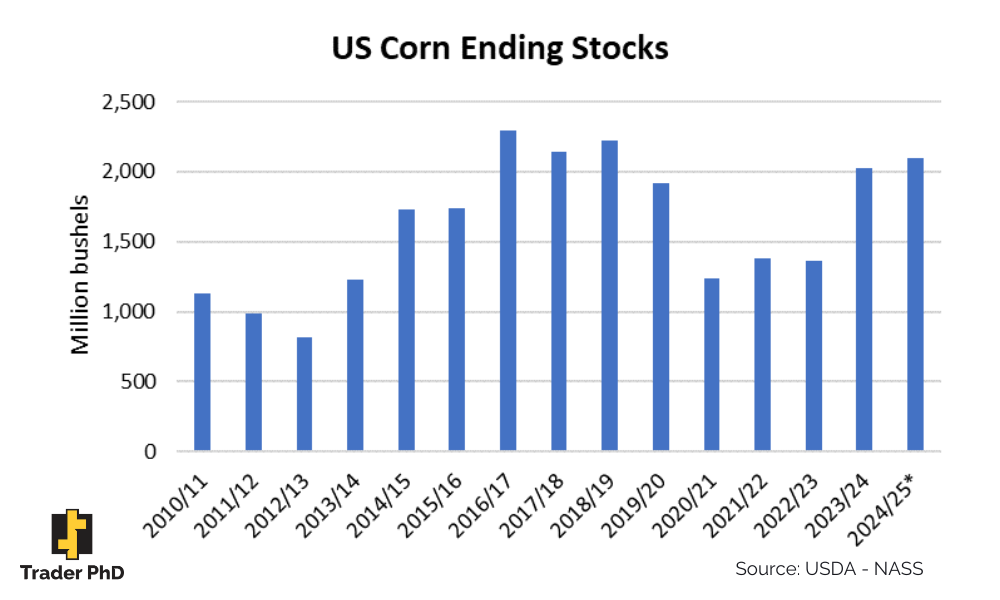

According to the USDA, we are expected to end the 2023/24 marketing year with a more than 2 billion bushel carryout. That is nearly 1 billion bushels more than the last two seasons after post-pandemic demand depleted U.S. supplies.

During the current marketing year, U.S. corn ending stocks have risen to the highest since the 2018/19 season, with forecasts for the next marketing year predicting an even higher carryout estimate. Additionally, the stocks-to-use ratio for corn, which is a representation of supply and demand trends, is at the highest level since the 2019/20 season.

But, just as high prices cure high prices, low prices can cure low prices. Supply concerns know how to spark a rally in the grain markets, but real sustained price support comes from demand. Corn exports, which are up about 30 percent as we round out the current marketing year, are also being complemented by stronger feed usage and ethanol processing.

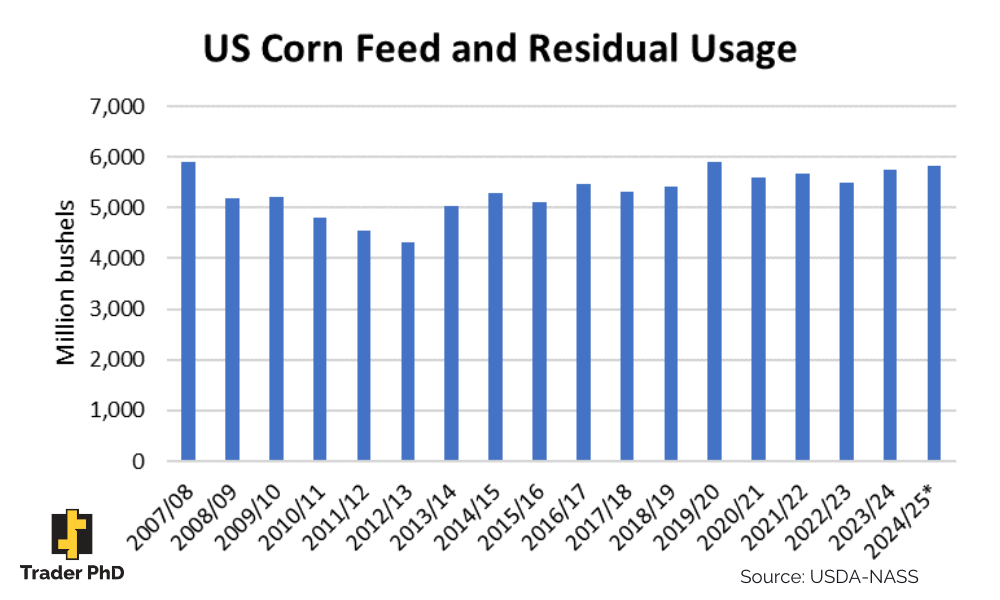

The USDA forecast feed and residual usage to climb to a five-year high next season. That comes as feedlots feed calves longer before sending them to slaughter and backfilling pens quicker with lighter feeder calves. For granted, the feed and residual usage category tends to be a catch-all for additional disappearances. However, current beef production data supports feeding trends as lower corn prices balance the economics of higher feeder and fed cattle prices.

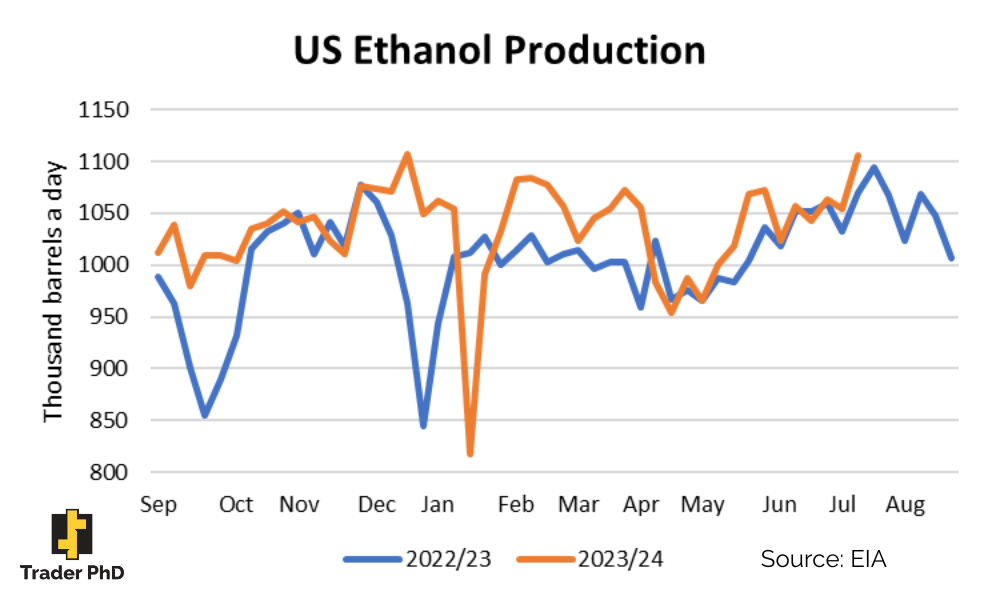

Weekly data from the Energy Information Administration has shown ethanol processing tracking above year-ago levels. So much so that the USDA raised its corn crush forecast multiple times throughout the season, with production expected to be the highest since 2018/19.

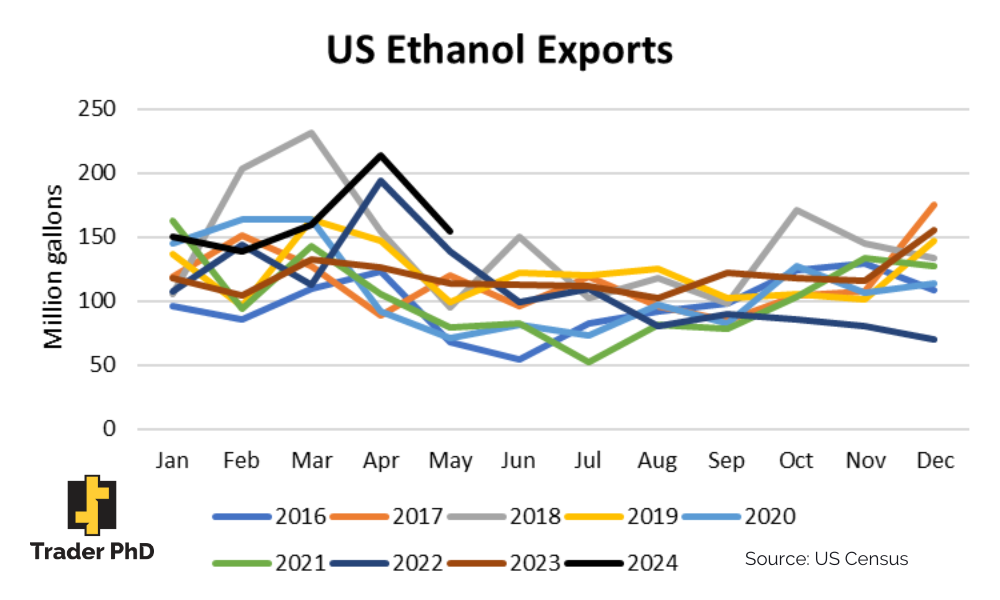

Data from the EIA shows that domestic gasoline consumption continues to struggle compared to previous years, leading to higher gasoline inventories, which could be negative for U.S. ethanol consumption. Despite lower domestic gasoline demand that would promote less blending, ethanol exports are helping to offset U.S. consumption. According to the USDA’s Foreign Agricultural Service, year-to-date exports through May are up 43 percent compared to the sale time last year and up 31 percent from the five-year average.

Canada is hungry for U.S. ethanol, and the United Kingdom, India, and Columbia are also notable buyers. New policies in Canada mandated increased use of fuel ethanol blends, with all gasoline to include at least 15 percent ethanol by 2030, which has been a primary driver of U.S. exports to the country.

While not much growth is expected for the ethanol industry, aside from the possible use of corn-based ethanol for sustainable aviation fuel production, ethanol is expected to remain a strong area for U.S. corn demand for the foreseeable future.

Year-to-date shipments for the marketing year may not be as strong as two seasons ago. Still, strong exports compared to last year are continuing to help chew through growing domestic supplies that could help the corn market begin to build a base that can better sustain prices.