.png?width=2347&height=620&name=outlined%20ag%20marketing%20logo%20black%20(1).png)

It’s no secret that U.S. soybean exports have been in the doldrums for the past year. Year-to-date exports for the current marketing year are well below last year, driven by increased supplies leaving South America, specifically Brazil.

Brazil is forecast to close out the current season with 100 million metric tons in exports, five percent higher year-over-year. Conversely, U.S. exports are expected to fall nearly 14 percent from last year.

That leaves more pressure on U.S. soybean crush to help pick up shortfalls.

U.S. Soybean Demand Dynamics

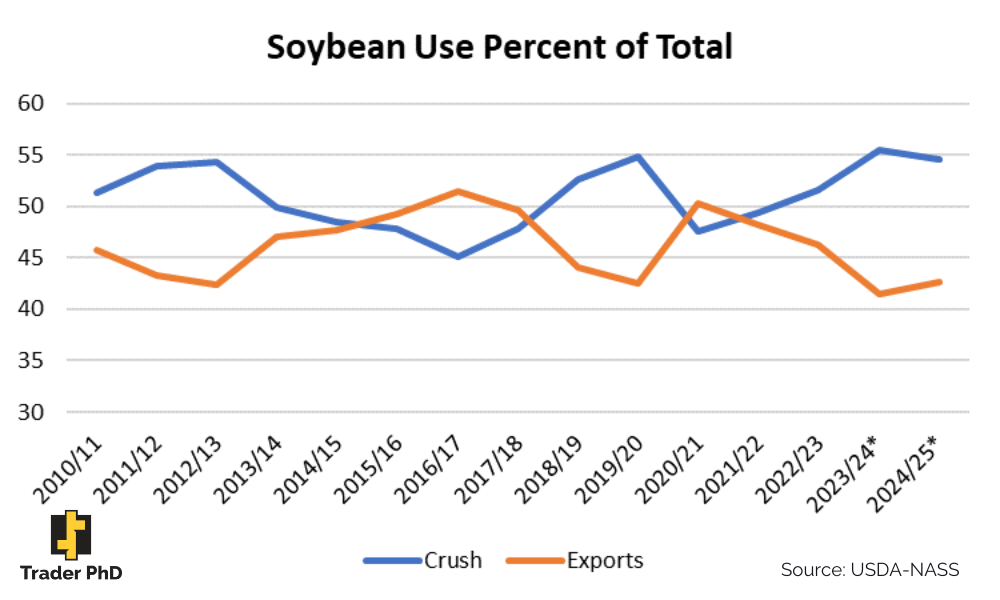

Demand dynamics for U.S. soybeans are broken down into two main categories - exports and crush. You have residual usage on the balance sheet, which counts more as a margin of error.

Whether by design or coincidence, the USDA’s data for whole soybean exports and crush volume have a perfect inverse relationship as a percent of total U.S. soybean usage.

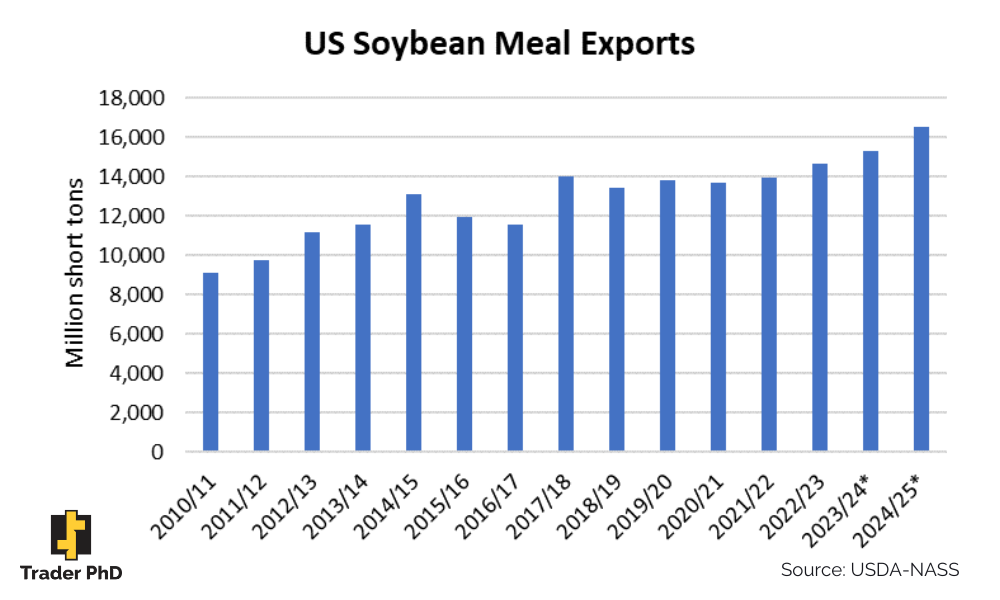

And what the chart conveys is that when either exports or crushings falter in a given year, the other tends to pick up much of the slack. Additionally, soybean demand has focused more on refined products over the last couple of years. Soybean crush benefited significantly from soybean meal exports, which continue to hit new records. Much of the growth over the last couple of years was due to a sharp drop in exports from Argentina due to drought. South American drought cut Argentina’s soybean output by half, digging into supplies available for processing. In turn, the U.S. boosted its exports, taking advantage of countries still wanting meal they couldn’t get from Argentina.

Soybean meal exports have been increasing steadily over the past 10 years. Even though Argentina’s soybean meal exports are expected to recover, the U.S. is forecast to have another record year for meal exports in the 2024/25 season - coming from data released during the USDA’s Agricultural Outlook Forum.

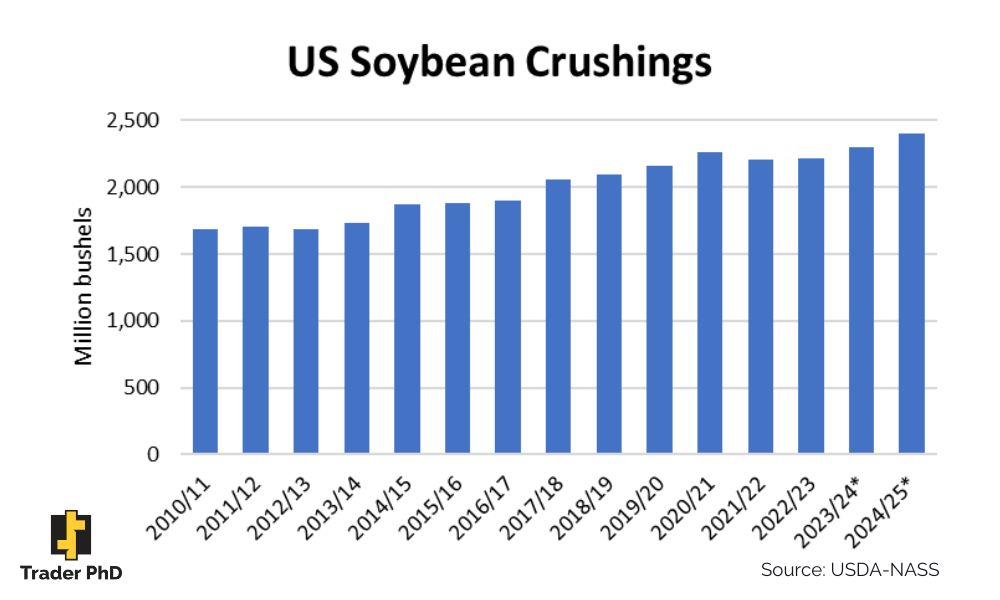

On the other side of the crush, soybean oil has been a bright spot for the industry. In a video released in September, we explored the Renewable Diesel boom and its role in soybean oil demand. The push for decarbonization across various sectors led to exponential growth in the soybean-based biofuels industry. That has led to the continual growth of U.S. soybean crushings. Crush expansion is expected to grow beyond this year’s record as companies remain optimistic about future demand.

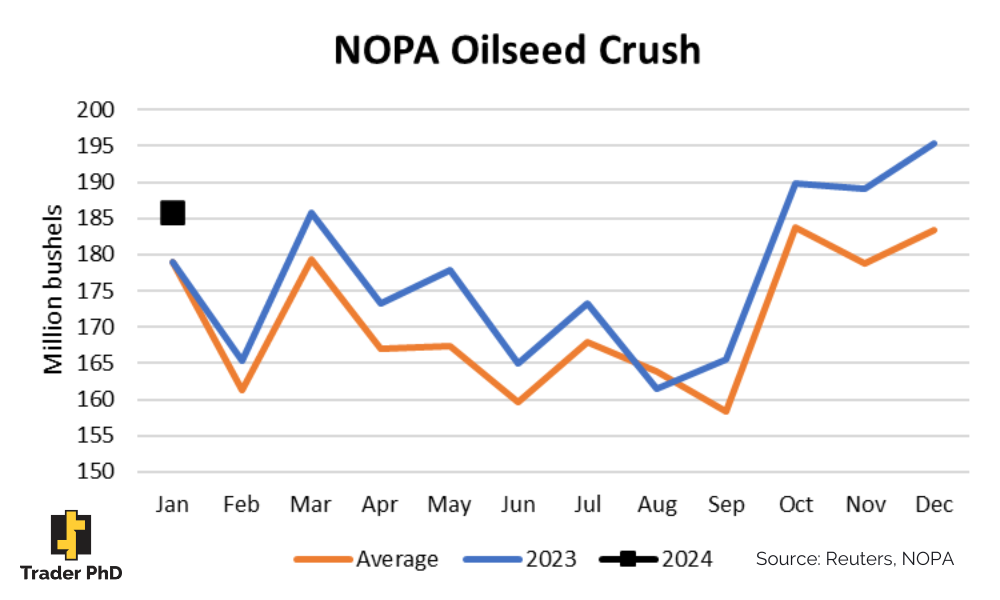

Recent data from the National Oilseed Processors Association confirmed the strong soybean crush demand that the USDA forecasts. Oilseed processors closed out January with soybean crushings reaching a new record for January of 189.7 million bushels. So, despite the slow export pace for soybeans, honing in on domestic crush and usage will likely be critical for filling in holes.

We already saw a shift from soybean oil being exported to primarily being used domestically. Does that mean we could see the same thing for whole soybeans as the U.S. ramps up soybean meal exports? Brazil is more competitive with whole soybean exports, but the U.S. has the advantage with soybean meal due to crush capacity - a capacity that continues to have expected future growth.

Another macroeconomic factor that could impact soybean exports is the potential of deglobalization. Trader PhD Founder and CEO Chad Toyne released a deglobalization audio broadcast series to subscribers in late January - part of which focused on agricultural trade. A deglobalized world could have many different impacts on international trade. And if that leads to fewer supplies leaving the United States - naturally or unnaturally, that could also emphasize the need for increased domestic usage.